- Home

- GST

- _IGST

- __Igst act

- __igst rules

- __Igst notification

- __igst circular

- _CGST

- __cgst act

- __cgst rules

- __cgst notification

- __cgst circular

- _UTGST

- __utgst act

- __utgst rules

- __utgst notification

- __utgst circular

- _gst composition

- __gst composition act

- __gst composition rules

- __notification

- __circular

- Income Tax

- _Income Tax Act

- _Income Tax Rules

- _Income Tax Notification

- _Income Tax Circulars

- _Updates

- Company Law

- Judgements

- Finance

- _Stock Market

- Services

- _GST

- _Income Tax

- _Account & Finance

- Buy Services

Showing posts from January, 2019Show All

MSME Act

MSME Act

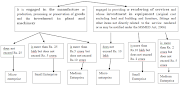

Analysis of Micro, Small & Medium Enterprises (MSME)

Analysis of Micro, Small & Medium Enterprises (MSME) Contains Enterpris…

Place of supply

Place of supply

Immovable Property Services under GST

Place of supply for Immovable Property Services under GST There is no definition …

gst update news

gst update news

Amendment to invoices of FY 17-18 in GSTR-1 has started on GSTN Portal

Amendment to invoices of FY 17-18 in GSTR-1 has started on GSTN Portal. Finally G…

ITC

Reversal of Input Tax Credit in case of Non-payment of Consideration

Reversal of Input Tax Credit in case of Non-payment of Consideration Input Tax Cre…

return for composition Schem

return for composition Schem

Details to be mentioned in GSTR-4

Details to be mentioned in GSTR-4 Return by Composition Dealer GSTR-4 is a GST R…

Waiver of late fee

Waiver of late fee for delay filing of GST returns

Waiver of late fee for delay filing of GST returns by GST Council The Central Gov…

Increase Exemption Threshold Limit

GST Update - Decisions taken by GST Council in its 32 Meeting on 10.01.2019

GST Update - Decisions taken by GST Council in its 32 Meeting on 10.01.2019 The GS…

Income Tax

Important Due date Compliance Calendar for January 2019

Important Due date Compliance Calendar for January 2019 Income Tax Act, 1961 07.…

RCM

GST Update New Services included in reversed charged (RCM) wef 01st Jan 2019)

GST Update New Services included in reversed charged (RCM) wef 01st Jan 2019) In …